“Bail-ins” are a relatively unknown risk associated with centralized banking that can be mitigated with consumer adoption of cryptocurrencies. Centralized banking is inherently risky for consumers and bail-ins are just the latest addition to its growing portfolio of risk. Cryptocurrencies, such as Bitcoin and Ether, can offer protections agains bail-ins. However, replicating existing banking models by merely switching fiat currency with cryptocurrencies leaves consumers exposed to similar risks.

What is a bail-in?

Unless you’ve been living under a rock, you know what is a bank bail-out. That is when the government “loans” tax-payer money to failed banks in order to cover losses, typically incurred through high-risk speculation. What you may not be aware of is an alternative solution to that problem: the bail-in.

…a bail-in, a term first popularised in the pages of The Economist, forces the borrower’s creditors to bear some of the burden by having part of the debt they are owed written off.

According to Investopedia, a bail-in is rescuing a financial institution on the brink of failure by making its creditors and depositors take a loss on their holdings. In certain instances, this is doubly painful for consumers because they twice take a haircut. The bank ends up taking all or a portion of the money that they have deposited into their checking and savings accounts and, if their pension funds have been invested with the same bank via relatively safe bonds, they lose part or all of that, as well.

At this point, you may be asking yourself how this is even possible. Part of it has to do with a little-understood feature of banking. Most people believe that when they deposit money into a bank account that the bank is merely holding their money for them. This is simply not the case. As soon as a person deposits money with the bank, that person is no longer the owner of the funds. Ownership has been transferred to the bank, of which the depositor has just become an an unsecured creditor. The bank issues a promissory note to its new creditor and now it is free to do whatever its wishes with its new money.

If one believes that one’s money is safer in the bank than it is underneath one’s mattress, then the banking relationship described above appears to be a fair exchange. However, this exchange is not without risk. And that risk appears to be growing.

The US has already put in place bail-in-like powers as part of the Dodd-Frank financial reform act passed last year. The law includes a resolution scheme that gives regulators the ability to impose losses on bondholders while ensuring the critical parts of the bank can keep running.

Employees would be paid, the lights would stay on and derivatives contracts would not have to be instantly unwound, one of the areas that caused market confusion when Lehman Brothers collapsed in September 2008.1

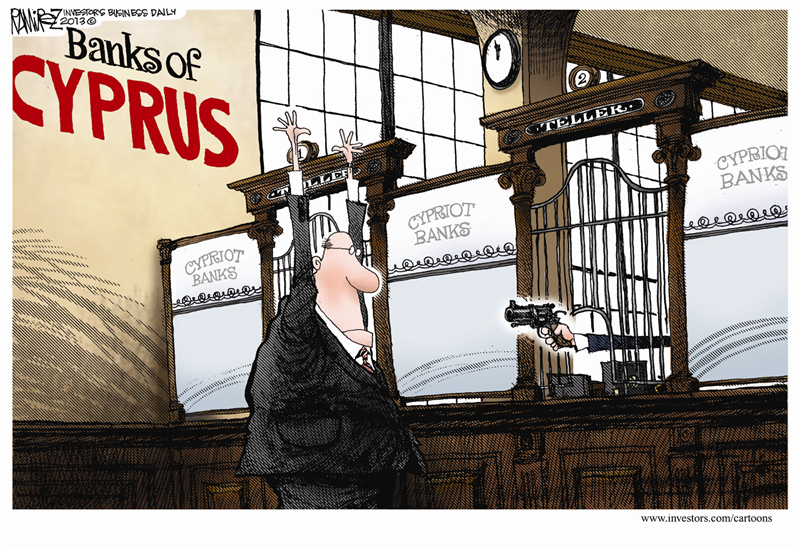

We have already witnessed the 2013 and 2015 bail-ins involving the Bank of Cyprus and several Italian banks, respectively. These were not one-offs. Evidently, bail-ins are the new, preferred bank rescue strategy in the European Union and the United States. In the US, this is possible due to a provision in the 2005 bankruptcy law that made derivatives liabilities more senior than depositors. This means that when a bank becomes insolvent and the line of debtors forms to collect their money, the derivative sellers get to be in the front of the line while the bank’s depositors get pushed to the back. As one might expect, the bank will have run out of money by the time it gets around to paying its depositors; which are unsecured creditors2. In 2016, the EU issued similar bail-in rules. A new term has entered the pop culture lexicon that captures this phenomenon. It’s called getting Cyprused.

Cryptocurrencies To The Rescue

Cryptocurrencies, such as Bitcoin and Ether, can offer protections against some of the risks inherent in traditional banking. Cryptocurrencies allow one to be one’s own bank. Though this is akin to storing money underneath your mattress, there are risk mitigation strategies that make self-banking a bit more practical and safe.

Bitcoin and cryptocurrencies, in general, are fundamentally peer-to-peer banking systems. They enable individuals to become their own banks. If you are your own bank, then there is no need to trust a third party. If you haven’t handed your money over to a third party then you are not at risk of losing your money due to institutional failure, either through a bail-in or bail-out. You are not at risk of being charged overdraft fees. You are also not at risk of the government taking your money without your knowledge when you store it in your private bitcoin wallet.

A bitcoin wallet is essentially a public / private cryptographic key pair within which value (BTC) can be stored on the blockchain. Bitcoin can be deposited into a wallet using the wallet’s public key. But bitcoin can only be removed from a wallet, or spent, using the wallet’s private key. Users typically store their bitcoins in a bitcoin wallet application. Bitcoin wallet applications come in one or more of three flavors: desktop, web, and mobile. In addition to wallet applications, there also exist paper wallets; which document the wallet’s public and private key on printed paper. In order to own and spend Bitcoin, you must be in possession of both the public and private keys.

This model of banking is not risk free, however. As with keeping fiat currency under the mattress, cryptocurrency users are responsible for securing their own money. On the one hand, you have to provide for the physical security of your money. If you store your cryptocurrency on your phone, then you have to make certain that your phone is not stolen. Further, the ability to spend cryptocurrency is dependent on access to private keys. You must also protect and remember your private keys otherwise, your money can be stolen or forever lost. There are a number of methods that can be employed in order to secure a bitcoin wallet, some of which include:

- Use 2-factor authentication

- Disconnect from the internet so that hackers cannot steal private keys

- Encrypt everything

- Use paper wallets

Nothing is 100% fool-proof but these methods can be employed to produce an acceptable level of risk with regards to protecting your cryptocurrency assets.

Or, Maybe Not

Simply using cryptocurrencies does not automatically protect one from classic banking risks. The risk posed by replicating existing banking models with cryptocurrencies is similar, if not greater. Leveraging third-party exchanges to store cryptocurrencies in much the same way as we use banks to store our cash involves similar third-party risk.

Bitcoin, as envisioned by Satoshi Nakamoto, is intended to be decentralized money. It is meant to be traded from person to person as anonymously as one might place fiat currency into the cup of a homeless person. It was never intended to be controlled by one or more centralized third parties.

The nearly half a billion dollar theft from and subsequent failure of Mt. Gox bears this out. A centralized repository of money on the internet represents a rich target for hackers. Further adding to the risk is that fact that there is very little regulation and oversight on these bitcoin exchanges in the US and internationally. So it is difficult to know whether the appropriate security measures matching the threat level have even been put in place. To this day, it is still unknown whether it was due to negligence or complicity. But 800,000 bitcoins were stolen from Mt Gox users. And since there is no FDIC equivalent for cryptocurrency exchanges, those users lost all of their money.

The recent situation at BitFinex was slightly different. The bitcoin exchange was hacked, much like Mt. Gox, and hackers got away with nearly 120,000 bitcoin ($60M at the time). The difference is that Bitfinex implemented a bail-in, forcing each customer to take a 36.067% haircut.

After much thought, analysis, and consultation, we have arrived at the conclusion that losses must be generalized across all accounts and assets. This is the closest approximation to what would happen in a liquidation context. Upon logging into the platform, customers will see that they have experienced a generalized loss percentage of 36.067%. In a later announcement we will explain in full detail the methodology used to compute these losses.

Bitfinex continues to operate, almost as if nothing ever happened.

Conclusion

Bail-ins can occur within any centralized financial institution where people deposit money or assets. This has started happening often enough that we call it getting “Cyprused” when a consumer loses his money in a bail-in. The bail-in, as a strategy, has been used to rescue a number of banks. And it has been used to rescue at lest one cryptocurrency exchange. The only way that consumers can defend against bail-ins is to use cryptocurrency in the way that it was meant. That is by using cryptocurrency to be one’s own bank.

1

Interestingly enough, commercial bank deposits would be completely unaffected by risky derivatives trading were Glass-Steagall still in force. The law required a firewall between commercial banks that hold customer deposits and investment banks that trade high-risk derivatives.

2

In the Cypriot bail-in, depositors were relieved of all funds they had on deposit over €100,000. In the United States, the FDIC insures bank deposits up to $250,000.

Resources

]]>